The automotive powertrain market size is expected to reach US$ 2,010.96 billion by 2031 from US$ 1,112.16 billion in 2024. The market is estimated to record a CAGR of 8.8% from 2025 to 2031.

The automotive powertrain market is broadly segmented by vehicle type into passenger cars, light commercial vehicles, and heavy commercial vehicles. Among these, the passenger car segment remains the most influential, accounting for a substantial share of global demand. The growth in this segment is propelled by increasing urbanization, rising disposable incomes in developing regions, and the broader trend toward personal mobility. Particularly in emerging economies, there has been a steady rise in vehicle ownership, driving demand for more efficient and environmentally friendly powertrain solutions. The traditional internal combustion engine continues to dominate in many regions, yet there is unmistakable momentum toward electrification and hybridization of vehicles, reflecting a broader market evolution.

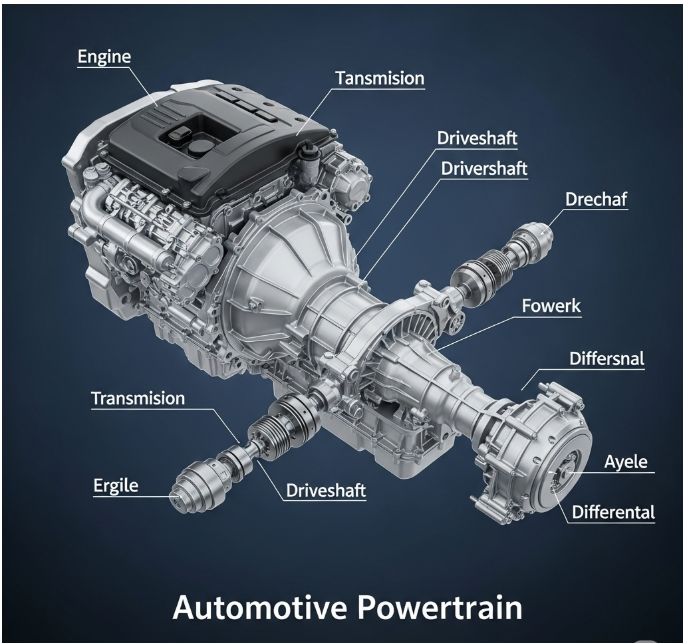

The Automotive Powertrain Market is experiencing significant transformation, driven by advancements in technology, changing regulatory frameworks, and evolving consumer preferences. This market encompasses the core components that generate power and deliver it to the road surface, including the engine, transmission, drive shafts, differentials, and final drive. With the global automotive sector shifting toward electrification, hybridization, and sustainable mobility, the Automotive Powertrain Market is adapting rapidly to meet new demands.

One of the primary growth drivers of the Automotive Powertrain Market is the rising adoption of electric vehicles (EVs) and hybrid electric vehicles (HEVs). Governments worldwide are enforcing stricter emissions regulations and offering incentives to encourage the use of cleaner energy sources. This shift is pushing manufacturers in the Automotive Powertrain Market to develop innovative systems that combine fuel efficiency with high performance. As a result, electric powertrains are gaining popularity, contributing to the overall growth and diversification of the Automotive Powertrain Market.

In parallel, internal combustion engines (ICEs) are also undergoing innovations to improve fuel efficiency and reduce environmental impact. Turbocharged engines, cylinder deactivation, and advanced fuel injection systems are some of the improvements being integrated into ICEs. These technological enhancements are helping the Automotive Powertrain Market maintain a strong foothold despite the surge in electric mobility solutions.

Another notable trend in the Automotive Powertrain Market is the growing demand for lightweight powertrain components. Automakers are increasingly using lightweight materials such as aluminum and composites to reduce vehicle weight and enhance fuel efficiency. This trend is not only shaping the future of vehicle design but also influencing the product development strategies within the Automotive Powertrain Market.

Furthermore, the market is witnessing increased investment in research and development aimed at optimizing transmission systems. Advanced automatic transmissions, continuously variable transmissions (CVTs), and dual-clutch transmissions (DCTs) are becoming more prevalent. These systems improve driving comfort and fuel economy, making them highly desirable in the modern Automotive Powertrain Market landscape.

https://www.businessmarketinsights.com/sample/BMIPUB00031628

Regional analysis of the Automotive Powertrain Market reveals that Asia-Pacific dominates the global market due to the presence of major automotive manufacturing hubs, particularly in China, Japan, and India. North America and Europe also contribute significantly to the Automotive Powertrain Market due to strong demand for high-performance vehicles and increasing investments in EV infrastructure.

The rise of connected and autonomous vehicles is another factor influencing the Automotive Powertrain Market. Smart powertrain systems that communicate with other vehicle components and infrastructure are being developed to enhance vehicle performance, safety, and efficiency. This digital integration is adding a new dimension to the Automotive Powertrain Market, creating opportunities for tech-driven innovations.

In conclusion, the Automotive Powertrain Market is poised for continued growth as it navigates the evolving landscape of mobility. Driven by environmental concerns, technological advancements, and changing consumer expectations, the Automotive Powertrain Market is set to play a pivotal role in shaping the future of the automotive industry. Stakeholders across the Automotive Powertrain Market are focusing on sustainability, efficiency, and innovation to remain competitive and meet the demands of tomorrow’s transportation ecosystem.

Executive Summary and Global Market Analysis:

The global automotive powertrain market is experiencing significant growth driven by stringent emission norms, rising consumer demand for EVs, and technological advancements. Automotive powertrain market on the basis of vehicle type encompasses passenger cars, light commercial vehicles, and heavy commercial vehicles. Passenger vehicles significantly influence the automotive powertrain industry, with market dynamics shaped by shifting user demands, environmental regulations, and innovative technologies. The passenger vehicle sector demonstrated continued expansion in 2024, propelled by heightened demand from developing markets, urban growth, and enhanced consumer purchasing power. The automotive powertrain industry, comprising traditional combustion engines (ICE) and electric vehicles (EVs), is experiencing fundamental changes

Automotive Powertrain Market Size and Share Analysis

The automotive powertrain market is classified according to vehicle into passenger cars, light commercial vehicles, and heavy commercial vehicles. The passenger car powertrain segment led the market in 2024 and beyond. Electric vehicles are showing remarkable momentum, with worldwide purchases expected to represent over 10% of car sales by 2025, driven by strict emission controls, state subsidies, and improved charging networks. European nations and China dominate electric vehicle uptake, while American markets show consistent expansion. Despite maintaining market leadership, traditional combustion engines face declining shares, especially in advanced economies, as automotive companies focus resources on electric technologies. Hybrid and plug-in vehicles provide transitional solutions, delivering improved fuel consumption and lower emissions, particularly attractive in areas with limited electric charging facilities. The powertrain sector benefits from innovations in lightweight components, turbocharging systems, and power-efficient solutions, enhancing combustion engine capabilities to satisfy emission requirements. Simultaneously, the declining cost of electric powertrains through production scaling and battery advancements enhances BEV competitiveness. However, the industry faces challenges due to supply network disruptions, battery material scarcity, and substantial initial EV costs. The Asia Pacific market leads in vehicle sales and powertrain manufacturing, with Chinese and Indian markets driving growth. As manufacturers pursue carbon neutrality targets, research in hydrogen fuel systems and eco-friendly production represents emerging trends, steering the powertrain industry toward an active transformation aligned with automotive electrification and sustainability objectives.

In terms of drive type, the market is segmented into front-wheel drive, rear-wheel drive, and all-wheel drive. The front-wheel drive (FWD) configuration continues to hold a substantial position in the worldwide automotive powertrain sector, especially for consumer vehicles and small commercial units, owing to its economical design, optimal space usage, and reduced fuel consumption. As of 2024, FWD layouts lead the small- and medium-sized vehicle categories, notably in city-focused regions such as Europe and Asia Pacific, propelled by the need for economical, productive transportation. The vehicle powertrain industry, including conventional engines (ICE), hybrid models (HEVs/PHEVs), and electric vehicles (BEVs), witnesses widespread FWD implementation across these propulsion types.

In terms of sales channel, the market is bifurcated into OEM and Aftermarket. The OEM segment emerged as the dominant sale channel in 2024. The Original Equipment Manufacturer (OEM) sales channel dominated the global automotive powertrain market in 2024, holding an estimated 68% share of the USD 1,112.16 billion market valued in 2024. This dominance is driven by robust vehicle production, particularly in China, which recorded 25 million vehicle sales in 2024, and India, with a 10.3% CAGR from 2019-2023. The OEM segment benefits from strong demand for internal combustion engine (ICE) powertrains, commanding an 88% share in 2024, alongside a surge in electric vehicle (EV) production, with global EV sales reaching 14 million units in 2023, up 35% YoY.

About Us-

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications.