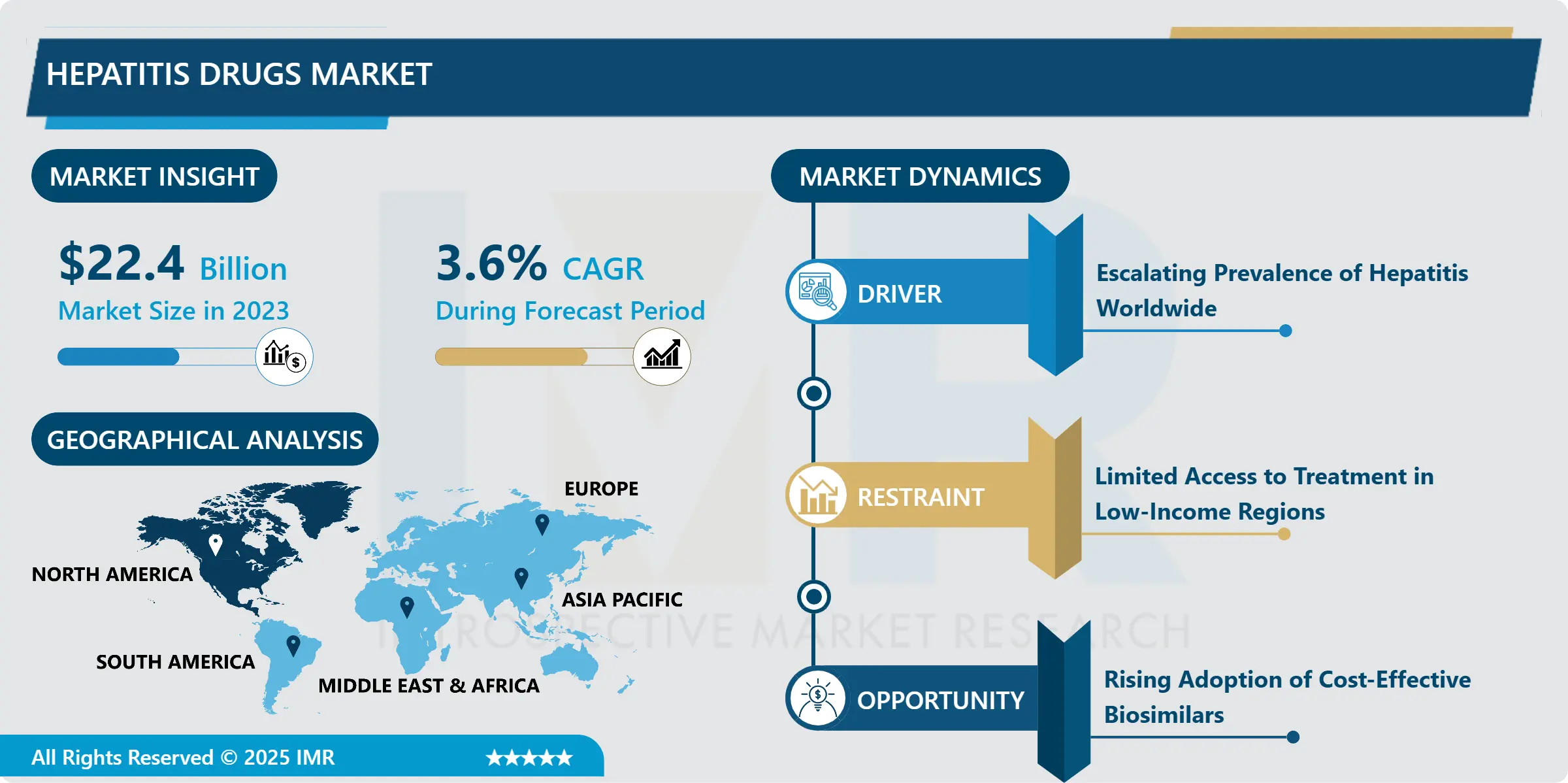

The global hepatitis drugs market is gaining importance as the prevalence of hepatitis infections continues to pose a major global health concern. These drugs are designed to reduce viral replication, prevent disease progression, and improve the quality of life for patients. Compared to traditional treatments, modern antiviral therapies offer higher cure rates, fewer side effects, and improved compliance. The market is primarily driven by rising awareness of hepatitis prevention and treatment, along with growing healthcare infrastructure across emerging economies.

Hepatitis drugs are a class of pharmaceutical products specifically developed to treat viral hepatitis, including types A, B, C, D, and E. These medications range from antivirals and immunomodulators to combination therapies, designed to suppress or eliminate the virus from the body. With advancements in biotechnology, newer classes of hepatitis drugs provide faster viral clearance and lower relapse rates. They are critical in preventing serious complications such as cirrhosis, liver failure, and hepatocellular carcinoma, making them indispensable in global healthcare.

Hepatitis Drugs Market, Segmentation

The Hepatitis Drugs Market is segmented on the basis of Drug Class, Distribution Channel, and Region.

Segment A: Drug Class

The drug class segment is further classified into Antiviral Drugs, Immunomodulators, and Combination Therapies. Among these, the Antiviral Drugs sub-segment accounted for the highest market share in 2023. Antiviral drugs are the cornerstone of hepatitis treatment, particularly for hepatitis B and C, due to their ability to directly target viral replication. They have become the preferred option owing to their higher success rate in preventing disease progression compared to traditional interferon-based therapies. With increasing clinical trials and the introduction of direct-acting antivirals (DAAs), this sub-segment continues to dominate.

Segment B: Distribution Channel

The distribution channel segment is further classified into Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies. Among these, the Hospital Pharmacies sub-segment accounted for the highest market share in 2023. This is largely due to the reliance on hospitals for diagnosis, initiation of treatment, and follow-up care for hepatitis patients. Hospital pharmacies are considered a trusted source for prescription-based antiviral drugs, ensuring compliance with treatment regimens. Additionally, the rising number of specialized liver care centers and advanced healthcare facilities worldwide has boosted the growth of this sub-segment.

One of the key growth drivers for the hepatitis drugs market is the rising global burden of hepatitis infections, particularly hepatitis B and C. The need for effective treatment options to prevent liver-related complications has fueled demand for advanced antiviral therapies and boosted market expansion.

A key market opportunity lies in the development of cost-effective generic hepatitis drugs. With patent expirations and increasing government focus on affordable healthcare, generic drug manufacturers are well-positioned to expand accessibility, especially in low- and middle-income countries where the disease burden is highest.

Some of The Leading/Active Market Players Are-

- Gilead Sciences, Inc. (USA)

- AbbVie Inc. (USA)

- Johnson & Johnson (USA)

- Bristol Myers Squibb (USA)

- Merck & Co., Inc. (USA)

- GlaxoSmithKline plc (UK)

- Cipla Ltd. (India)

- Roche Holding AG (Switzerland)

- Aurobindo Pharma (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Mylan N.V. (USA)

- Zydus Lifesciences Ltd. (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Novartis AG (Switzerland)

and other active players.

Key Industry Developments

In March 2024, Gilead Sciences received FDA approval for an expanded indication of its hepatitis C drug for pediatric patients.

This approval marks a significant step in extending effective antiviral treatment to younger age groups, highlighting the company’s commitment to addressing unmet medical needs in vulnerable populations.

In July 2023, AbbVie launched a generic version of its hepatitis C therapy in select emerging markets to increase affordability.

The introduction of generics in cost-sensitive regions aims to expand treatment access, reduce healthcare costs, and support global initiatives for hepatitis elimination by 2030.

Conclusion

The global hepatitis drugs market is expected to show steady growth, reaching USD 30.79 billion by 2032. Rising awareness, expanding access to treatment, and the development of advanced antiviral therapies remain pivotal factors driving the market. While challenges like affordability persist, the increasing adoption of generics and strong government healthcare initiatives present significant opportunities. With major pharmaceutical companies actively investing in R&D, the market is well-positioned to support global efforts in reducing the burden of hepatitis infections and improving public health outcomes.

Browse Complete Summary and Table of Content @ https://introspectivemarketresearch.com/reports/hepatitis-drugs-market